The Economist: Currency unions in Africa

The Economist has a very interesting article on the growing number of currency unions in Africa. It talks about the differences between the unions, their chances for the future and of course, being The Economist, their biggest threats.

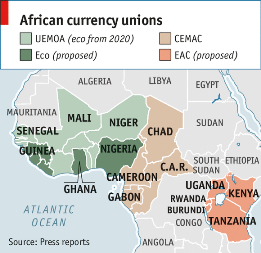

THE euro crisis has put most people off currency unions. But not in Africa, it seems. In November the leaders of five countries of the East African Community (EAC) agreed to form a monetary union within ten years. A month before West African politicians agreed on a plan to introduce a new shared currency, the eco, over the next few years. It should eventually subsume West Africa’s existing currency bloc—but not its central African cousin.

THE euro crisis has put most people off currency unions. But not in Africa, it seems. In November the leaders of five countries of the East African Community (EAC) agreed to form a monetary union within ten years. A month before West African politicians agreed on a plan to introduce a new shared currency, the eco, over the next few years. It should eventually subsume West Africa’s existing currency bloc—but not its central African cousin.

Under the proposal an initial group of six countries will adopt the eco by 2015 (see map). Five years later the members of the West African Economic and Monetary Union (known as UEMOA, its French acronym), which currently share a currency called the West African CFA franc, are to adopt the eco too, creating a currency union of over 300m people.

West African politicians are pushing for further integration because they, like most economists, argue that the single currency for UEMOA has been a qualified success. UEMOA member states are more fiscally disciplined than their neighbours outside the currency zone, says Cécile Couharde of the University of Paris Ouest Nanterre La Défense. The French government currently underwrites the West African CFA franc by guaranteeing to convert it to euros at a ratio of one to 0.0015. That has provided a stability rare in African currencies. Monetary unions also simplify trade: UEMOA has more intraregional trade than any other region in Africa, according to an IMF paper.

But the currency union has downsides. UEMOA economies move at different speeds. According to research by Romain Houssa, at the Catholic University of Leuven in Belgium, economic changes are poorly correlated between member states. From 2007 to 2012, the IMF found, the correlation between the business cycle of Senegal, a country with strong trade links outside the zone, and the other countries in UEMOA was almost zero.

Consequently, a UEMOA-wide interest rate is not ideal: as in the euro zone, some countries end up with the wrong rate. And an inflexible exchange rate makes economic adjustment difficult. From 2000 to 2012 average annual growth in output in UEMOA countries was about half that of comparable sub-Saharan economies, according to Gianluigi Giorgioni of Liverpool University.

Whereas UEMOA’s currency union has drawbacks, the proposed eco zone may have fatal flaws. It would encompass even more economic diversity. Nigeria in particular stands out. Its economy is huge by its neighbours’ standards. UEMOA’s GDP is about $75 billion; Nigeria’s is about $260 billion. The GDP of the next-biggest economy in the region, Ghana, is about $40 billion. And the Nigerian economy is unusual. Unlike most other West African countries it is heavily dependent on oil, which accounts for over a third of output, according to data from the OECD, a club of mostly rich countries.

IMF research shows that Nigeria’s balance of trade tends to move in the opposite direction to its neighbours’—they are largely importers of oil. During periods of high oil prices Nigeria may push for interest-rate rises. That would be disastrous for other eco-zone economies, which are likely to be gasping for lower rates.

To make matters worse the eco might be vulnerable to speculative attack. France would be unlikely to guarantee it, reckons Mr Giorgioni, as the liabilities would be large and the countries involved are not former French colonies. Without such support, investors would be nervous. Any fiscal laxity would be punished. If a region as rich as the euro zone has struggled to cope with such pressures, the likelihood that the poorer and less well-governed places hoping to adopt the eco could is tiny.

(© The Economist)

No comments